⤴️-Paid Ad- Check advertising disclaimer here. Add your banner here.🔥

All Activity

- Past hour

-

Can u share the settings

-

You can still view the settings. Save the template then click on the gear to see the settings.

-

Parthh joined the community

Parthh joined the community - Today

-

⭐ traderwin reacted to a post in a topic:

livewireindicators.com

⭐ traderwin reacted to a post in a topic:

livewireindicators.com

-

⭐ traderwin reacted to a post in a topic:

livewireindicators.com

-

⭐ traderwin reacted to a post in a topic:

livewireindicators.com

-

⭐ traderwin reacted to a post in a topic:

livewireindicators.com

-

Welcome to Indo-Investasi.com. Please feel free to browse around and get to know the others. If you have any questions please don't hesitate to ask.

-

⭐ RichardGere reacted to a post in a topic:

Please, I want Amibroker 6,43 64bit

-

If anyone can provide the setup for amibroker v7 beta I am sure I can fix it for you. please provide. preferably x64 version thanks

-

mickeyg819 joined the community

mickeyg819 joined the community -

Hello , I came across an order flow package that is very similar to MZ pack and has limit order histogram similar to bookmap , i am posting the file that on their website , maybe someone can educate this https://clusterdelta.com/ninjatrader-bookmap ClusterDelta_NinjaTrader8.zip

Hello , I came across an order flow package that is very similar to MZ pack and has limit order histogram similar to bookmap , i am posting the file that on their website , maybe someone can educate this https://clusterdelta.com/ninjatrader-bookmap ClusterDelta_NinjaTrader8.zip -

HFMarkets (hfm.com): Market analysis services.

AllForexnews replied to AllForexnews's topic in Fundamental Analysis

Date: 28th November 2025. Three Critical December Events That Will Shape Gold and the US Dollar. November has been one of the few months where Gold and the US Dollar have simultaneously risen in value. Over the past 30 days Gold has risen 4.00% and the US Dollar by 1.15%. However, since 1 November the US Dollar has outperformed the precious metal. The two instruments rarely rise simultaneously in value due to the inverse correlation. However, the US shutdown has made it possible for both assets to advance. Traders are now reassessing the outlook for both assets over the next one to two months, noting that both are unlikely to keep rising. Economists tend to support that one of the two tends to give way for the other to continue increasing. The performance of the US Dollar Index and Gold will almost entirely depend on the next three days. US Dollar Index 12-Hour Chart 10 December On 10 December, the Federal Reserve will make its decision on interest rates for the last time in 2025. The decision will be made three days after the release of the US Core PCE Price Index, therefore, their decision will also depend on this release. However, the US Core PCE Price Index has not seen any shocking releases over the past few months. Currently, economists and investors are almost certain that the Federal Reserve will cut interest rates by 0.25%. According to the Chicago exchange, almost 80% of market participants believe the Fed will cut interest rates. The exchange also notes that 24% of traders believe the Fed will cut again in January 2026. If the Federal Reserve cuts rates in December, Gold is likely to gain further, particularly if FOMC members point to economic or employment weakness. Simultaneously, the US Dollar Index may decline. Due to the rate adjustment already, economists and large institutions will largely be focused primarily on commentary about future rate adjustments. This is likely to be the biggest price driver, but the upcoming NFP figures may change how the Fed views interest rates in the first quarter of 2026. 16 December This is likely to be the most volatile day for the US Dollar Index, Gold and US indices. Due to the government shutdown, the previous NFP data had not been made public. On 16 December, the US will release the NFP Employment Change for both October and November. The release is a rare event where the US releases two months worth of data at once. If the NFP report shows rising unemployment and weak job creation, the Federal Reserve may consider a larger rate cut. This could potentially include a 50-basis-point cut in January 2025. If the data is weak but the Fed does not opt for a larger cut, it will likely move towards smaller but more frequent rate reductions. Another reason why 16 December is likely to be the most volatile day of the year is that, in addition to the NFP releases, the US will also publish its PMI data and ADP Weekly Employment Change. Therefore, investors will have plenty of data to analyse and digest. The most impactful news will be the NFP release, Unemployment Rate, PMI reports, Average Salary Earnings and then the ADP Weekly Employment Change. 18 December Only two days after the NFP release, markets are likely still adjusting their portfolios to reflect the new economic outlook, meaning volatility may remain elevated. However, the US is also set to publish its latest Consumer Price Index. Which will provide fresh insight into affordability, demand, and the Federal Reserve’s next steps. If inflation reads lower than expectations or in line with expectations, Gold could potentially witness higher demand. Whereas, higher inflation paired with a cautious Fed would support the US Dollar. Gold (XAUUSD) If the new releases support a dovish Federal Reserve for the first quarter of 2026, the price of Gold may potentially rise. Possible targets include price ranges between: $4,381.30 and $4,555.00 HFM-Gold Daily Chart US Dollar Index On the other hand, if the Federal Reserve is likely to opt for a prolonged pause due to higher inflation data and strong employment figures, the US Dollar potentially may rise instead of Gold. In that case, Gold may potentially fall to prices between $3,831.00 and $3,605.50 Key Takeaway Points: Gold and the US Dollar rose together in November, but both are unlikely to continue climbing in the coming months. Markets expect a Fed rate cut on 10 December, with guidance on future policy being the main focus. 16 December could be highly volatile, with two months of NFP data released alongside major economic reports. Weak NFP figures may push the Fed toward larger or more frequent cuts, supporting Gold and pressuring the Dollar. The 18 DecemberCPI release will guide early-2026 expectations and determine whether Gold or the Dollar gains momentum. Always trade with strict risk management. Your capital is the single most important aspect of your trading business. Please note that times displayed based on local time zone and are from time of writing this report. Click HERE to access the full HFM Economic calendar. Want to learn to trade and analyse the markets? Join our webinars and get analysis and trading ideas combined with better understanding of how markets work. Click HERE to register for FREE! Click HERE to READ more Market news. Michalis Efthymiou HFMarkets Disclaimer: This material is provided as a general marketing communication for information purposes only and does not constitute an independent investment research. Nothing in this communication contains, or should be considered as containing, an investment advice or an investment recommendation or a solicitation for the purpose of buying or selling of any financial instrument. All information provided is gathered from reputable sources and any information containing an indication of past performance is not a guarantee or reliable indicator of future performance. Users acknowledge that any investment in Leveraged Products is characterized by a certain degree of uncertainty and that any investment of this nature involves a high level of risk for which the users are solely responsible and liable. We assume no liability for any loss arising from any investment made based on the information provided in this communication. This communication must not be reproduced or further distributed without our prior written permission. -

fxtrader99 reacted to a post in a topic:

Ninza Williams Fractal Pro & Ninza DWIN Reversal

-

I DON'T KNOW WHAT IT IS, I WAS LOOKING FORWARD TO IT AND THEN I WAS DISAPPOINTED.

-

Chidiroglou reacted to a post in a topic:

Sonarlike Iceberg Finder

Chidiroglou reacted to a post in a topic:

Sonarlike Iceberg Finder

-

same thing with me. is this educ?

-

mabrouk joined the community

mabrouk joined the community -

TraderMan reacted to a post in a topic:

iFVG Autotrader - Timeless Trading

TraderMan reacted to a post in a topic:

iFVG Autotrader - Timeless Trading

-

Yes only ats members can see the settings in tradingview, @dex can you please share them via screenshots

-

I’ve settled on risking less than 1% per idea and only scale up after a statistically significant edge shows up in my journal; the smaller risk kept me in the game long enough to learn

-

Dimdium reacted to a post in a topic:

Tremper.com

-

The indicator can be seen among the indicators but does not appear in the chart.

-

-

In my own practice with HFM, I only moved to micro-lots after a few months of demo + webinar replays and a journal showing I could stick to my rules, not just hit random wins. That slow transition helped a lot with keeping fear and greed under control once real money was on the line

-

XandarT reacted to a post in a topic:

NINZA Bo$$ Order Block

-

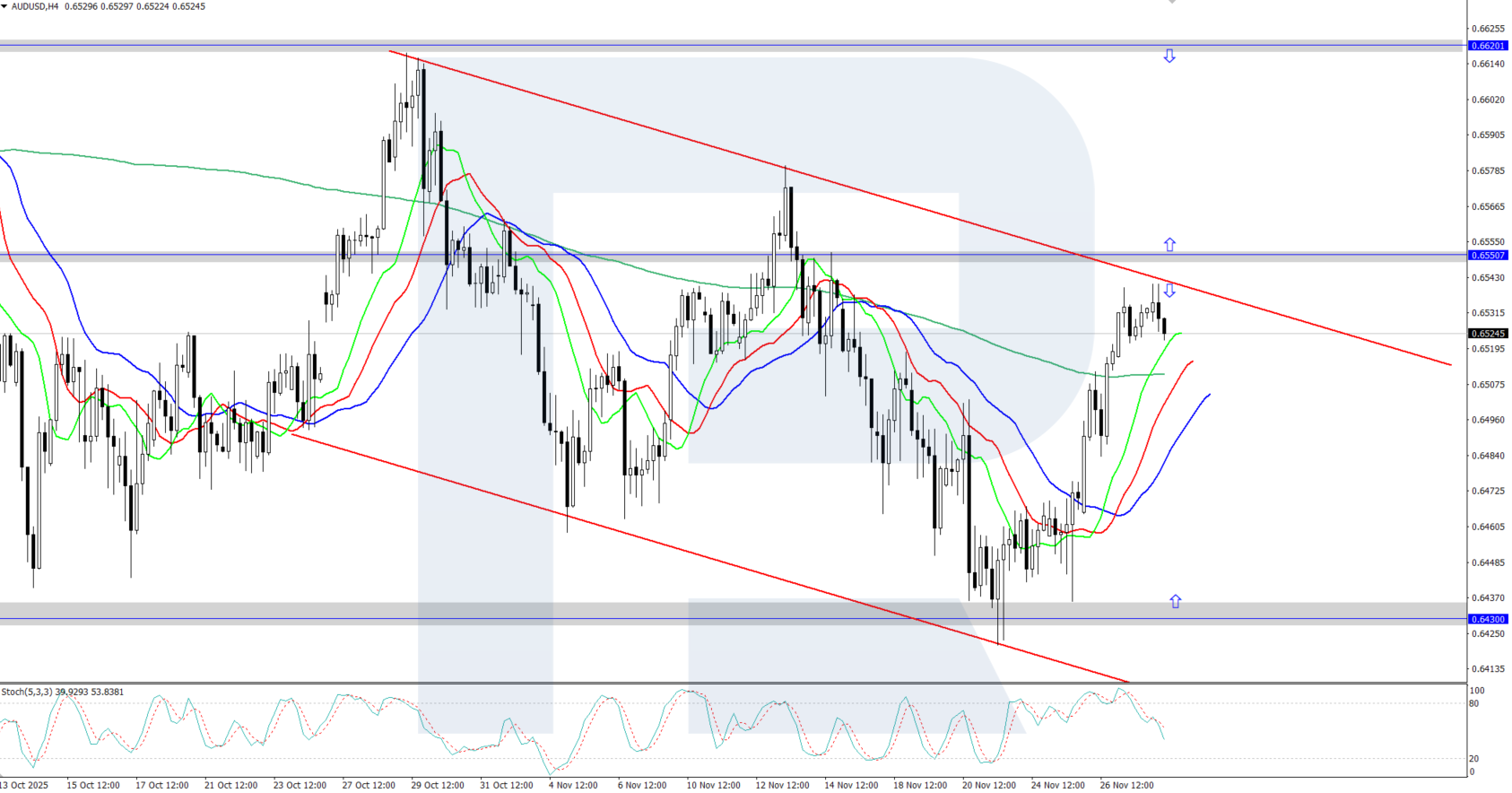

Market Technical Analysis by RoboForex

RBFX Support replied to RBFX Support's topic in Technical Analysis

AUDUSD climbed above 0.6500 The AUDUSD rate is moderately rising, having consolidated above the 0.6500 level. The Reserve Bank of Australia does not plan to cut rates in the near term. Discover more in our analysis for 28 November 2025. AUDUSD technical analysis The AUDUSD pair is showing solid growth after reversing upwards from the daily support level at 0.6430. The Alligator indicator is pointing upwards, confirming bullish momentum. The key resistance level is 0.6550. The AUDUSD pair is rising moderately, consolidating above 0.6500. Read more - AUDUSD Forecast Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews. Sincerely, The RoboForex Team

-

roboforex Market Fundamental Analysis by RoboForex

RBFX Support replied to RBFX Support's topic in Fundamental Analysis

Falling inflation in Germany breaks EURUSD forecasts The euro, attempting to regain lost ground, has slowed its upward momentum, with the EURUSD pair trading near 1.1580. Find out more in our analysis for 28 November 2025. EURUSD forecast: key trading points Germany’s Consumer Price Index (CPI): previously at 0.3%, projected at -0.2% Markets await the Fed’s interest rate decision EURUSD forecast for 28 November 2025: 1.1540 Fundamental analysis The EURUSD forecast takes into account that today the euro, after attempting to regain lost ground, is forming a correction, with the pair trading near 1.1580. Germany’s Consumer Price Index reflects changes in the cost of goods and services for consumers, helping to assess purchasing trends and the degree of economic stagnation. A lower-than-expected reading will have a negative impact on the European currency. RoboForex Market Analysis & Forex Forecasts Attention! Forecasts presented in this section only reflect the author’s private opinion and should not be considered as guidance for trading. RoboForex bears no responsibility for trading results based on trading recommendations described in these analytical reviews. Sincerely, The RoboForex Team -

NQ Ultra - Futures Trading Bot // https://tradegreater.com/

Night replied to luludulu's topic in Ninja Trader 8

Does anyone see new version 3.4.8 available on whop or is it still 3.4.7? -

Welcome to Indo-Investasi.com. Please feel free to browse around and get to know the others. If you have any questions please don't hesitate to ask.

-

ThreeBeast joined the community

ThreeBeast joined the community -

They cannot break it. Nobody could break it, I lost mine already. If you break it , you will be in the FBI 10 most wanted list. Use Coinbase , they give your account free right to connect to NT 8

-

Ok, looks like the settings are in the tradingview links as playr101 said

-

Ninza Williams Fractal Pro & Ninza DWIN Reversal

omni69 replied to ngatho254's topic in Ninja Trader 8

Thanks @ngatho254, That worked. What happens if I import a different Ninza indicator that comes with its own resource file? - Yesterday

-

@dex can you goto the tradingview charts for Velociraptor, Timid Raptor, and OG Raptor and screenshot each of their settings, then post here? Can't see the settings if not subscribed. Velociraptor - https://www.tradingview.com/chart/EndV38TY/ OG Raptor - https://www.tradingview.com/chart/CWmS4bR5/ Timid Raptor - https://www.tradingview.com/chart/UGq0eu79/ even better if there are NT8 .xmls available. But whatever works to get the right settings.

-

Welcome to Indo-Investasi.com. Please feel free to browse around and get to know the others. If you have any questions please don't hesitate to ask.

-

would love to get these cracked, this is the website https://ninjatools.studio/

-

Ninza Williams Fractal Pro & Ninza DWIN Reversal

ngatho254 replied to ngatho254's topic in Ninja Trader 8

@omni69 remove all the other ninza indicators or replace the resource file with what was uploaded with the files